"Jake - Has Bad Luck So You Don't Have To" (murdersofa)

"Jake - Has Bad Luck So You Don't Have To" (murdersofa)

11/14/2018 at 10:08 • Filed to: None

0

0

41

41|

"Jake - Has Bad Luck So You Don't Have To" (murdersofa)

11/14/2018 at 10:08 • Filed to: None | 0

| 41 |

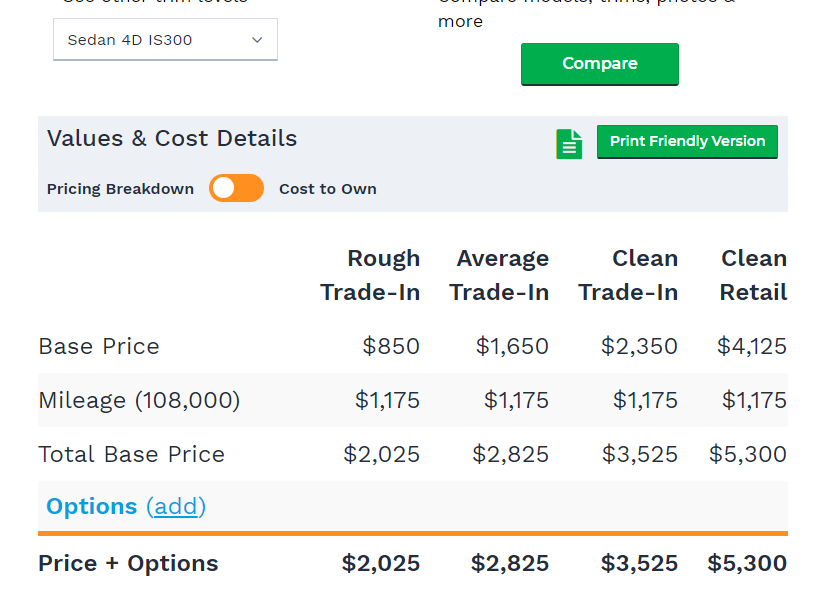

Insurance appraiser called last night and said the lexus may be totaled. N E A T. Dunno what I’ll do if that’s the case.

Here’s the fun part: A clean 2002 IS300 sedan values at $5,300. About right.

NADA thinks the wagon is only worth $212 more which is patently horseshit.

150k miles ‘04 for $6500:

!!! UNKNOWN CONTENT TYPE !!!

208k miles salvage title ‘02 for $4700:

!!! UNKNOWN CONTENT TYPE !!!

205k miles ‘02 for $4895:

!!! UNKNOWN CONTENT TYPE !!!

223k miles ‘02 salvage title for $4500:

!!! UNKNOWN CONTENT TYPE !!!

172k mile ‘02 for $7000

!!! UNKNOWN CONTENT TYPE !!!

199k ‘02 for $7900

!!! UNKNOWN CONTENT TYPE !!!

This is the closest to mine: 107k mile ‘02 for $6900

!!! UNKNOWN CONTENT TYPE !!!

101k ‘05 for $10k

!!! UNKNOWN CONTENT TYPE !!!

127k ‘04 with body damage for $5500

!!! UNKNOWN CONTENT TYPE !!!

Rusty 150k ‘03 for $5000

!!! UNKNOWN CONTENT TYPE !!!

So yeah. $5,500 for a clean sportcross with 108 k miles and no prior body damage is absolute bullshit.

Dr. Zoidberg - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

Dr. Zoidberg - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:25 |

|

Yep, I had a feeling you’d get fucked. Last month when I went on CarGurus, there were TWO for sale nationally. One had 100k miles listed for $11,000...

HFV has no HFV. But somehow has 2 motorcycles

> Jake - Has Bad Luck So You Don't Have To

HFV has no HFV. But somehow has 2 motorcycles

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:25 |

|

If they total it, I would buy it out and keep driving it the way it is, as it look to be pure cosmetic damage .

Arrivederci

> Jake - Has Bad Luck So You Don't Have To

Arrivederci

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:26 |

|

You’re absolutely going to get fucked if you want the insurance money. They only pay ACV, which is basically black book. Figure out what it’s worth as a trade-in, and that’s probably what they’ll pay. It’s a bullshit practice.

Long_Voyager, Now With More Caravanny Goodness

> Jake - Has Bad Luck So You Don't Have To

Long_Voyager, Now With More Caravanny Goodness

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:28 |

|

Take the money, fix it yourself.

The Dummy Gummy

> Jake - Has Bad Luck So You Don't Have To

The Dummy Gummy

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:28 |

|

What’s wrong with it? If it isn’t structure, take the totaled pay out and keep the car.

|

Jake - Has Bad Luck So You Don't Have To

> Long_Voyager, Now With More Caravanny Goodness

11/14/2018 at 10:30 |

|

Will still be salvage title. Very difficult to insure and I’m not sure I could get full coverage on it.

|

Jake - Has Bad Luck So You Don't Have To

> The Dummy Gummy

11/14/2018 at 10:31 |

|

Front clip needs replaced. I’m unsure what the situation is with insuring a rebuilt title car.

|

Jake - Has Bad Luck So You Don't Have To

> Arrivederci

11/14/2018 at 10:31 |

|

I just went through this with my Miata. Insurance is a fucking scam.

|

Jake - Has Bad Luck So You Don't Have To

> HFV has no HFV. But somehow has 2 motorcycles

11/14/2018 at 10:32 |

|

So it sounds super shallow because it is but I can’t mentally handle that. I worked my ass off all summer and rode a bike to work to afford to _finance_ this fucking thing because I wanted a really nice car that I could be proud of, be reliable, and not have to worry about. now it’s none of those things and I can’t take it.

|

Jake - Has Bad Luck So You Don't Have To

> Dr. Zoidberg - RIP Oppo

11/14/2018 at 10:32 |

|

Yep. Yay me.

|

HFV has no HFV. But somehow has 2 motorcycles

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:33 |

|

I completely understand. I have a feeling I’d feel the same about the BMW.

|

Arrivederci

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:35 |

|

Massive scam, but like HFV said, if they total it, take the shitty amount of money they give you and buy it back. You should have enough left over to get it properly repaired, but it’ll have that mark on its title. That said, you still know its history and know how little damage it actually had, so it’ll still be a good car and look great. Just document the damage and repairs really well in case you ever want to sell it. I wouldn’t be afraid of buying this car if it was properly repaired.

|

The Dummy Gummy

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:37 |

|

I haven’t done it but a friend has, it’s a little pricier for some reason with the insurance for others, but you can remove the pay out for your car which makes it cheaper over all.

themanwithsauce - has as many vehicles as job titles

> Jake - Has Bad Luck So You Don't Have To

themanwithsauce - has as many vehicles as job titles

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:41 |

|

Contact your lender. They have a vested interest in you getting the proper value of the car. Explain what’s happening and see if they can send some documents showing that they agree the value of the vehicle is higher. I assume if you got a loan, there is a lien on the title of the car?

|

Jake - Has Bad Luck So You Don't Have To

> themanwithsauce - has as many vehicles as job titles

11/14/2018 at 10:43 |

|

Oh, good thought. And yes there’s a lien.

Akio Ohtori - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

Akio Ohtori - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:44 |

|

If it were me and I really liked the car and the adjuster isn’t a prick, I’d ask what your options are. If you’re willing to take the maximum non-totaled payout and do the rest out of pocket, that might be an option?

I dunno. When my neighbor backed into the Disco I just told my body shop to do what they had to do so it wasn’t totaled. They managed to straighten the fender without replacing it, replaced a mount on the headlight instead of the whole assembly and I ended up giving the shop some parts that I had previously purchased anyway.

Worked out but your mileage may vary.

|

Jake - Has Bad Luck So You Don't Have To

> Akio Ohtori - RIP Oppo

11/14/2018 at 10:49 |

|

The problem here is the bank owns the car. Lessens my options somewhat.

punkgoose17

> Jake - Has Bad Luck So You Don't Have To

punkgoose17

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:50 |

|

If they do total it do they give you $5,512? You can buy it back for $2,162? And, it still has a market value of $5,500 with an R title?

You are right their evaluation is wrong.

|

Akio Ohtori - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:52 |

|

Ahh. I mean... do they really have a dog in this fight as long as they get their oh I get it. Yeah that could complicate things. Rare and older cars are always a gamble with insurance, unfortunately . I’d work the insurance and body shop to see if they can help out, if the car is important to you. Otherwise well... that sucks.

|

Dr. Zoidberg - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 10:52 |

|

I agree with your assessment. The whole point of the car was that it was a nice car.

|

Jake - Has Bad Luck So You Don't Have To

> punkgoose17

11/14/2018 at 11:07 |

|

The bank owns it. I owe something like $5,500 on it so if they don’t pay at least that it just goes bye bye.

|

Dr. Zoidberg - RIP Oppo

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 11:07 |

|

If the buy-back is cheap and you can’t get more money, I would part it out. Grille, headlights, tail lights, hatch are all easy items.

|

Jake - Has Bad Luck So You Don't Have To

> Dr. Zoidberg - RIP Oppo

11/14/2018 at 11:16 |

|

Bank owns it. Not sure what the situation is there.

|

The Dummy Gummy

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 11:24 |

|

Just noticed from the other comments it has a lien. You won’t be able to go the route I suggested with a lien on the car. Banks require full coverage. Sorry brotha.

|

themanwithsauce - has as many vehicles as job titles

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 11:54 |

|

Yeah, then their own actuary tables probably say the vehicle has a high enough value to justify the loan you got. If at all possible, try and get out of being the middleman and just get the insurance people talking to the loan people.

|

Long_Voyager, Now With More Caravanny Goodness

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 12:14 |

|

If it’s difficult to insure it’s because of your carrier, not the car. I’ve owned plenty of “salvage” title vehicles and never had an issue insuring them, even with full coverage.

|

themanwithsauce - has as many vehicles as job titles

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 12:16 |

|

Oh holy fuck, yeah get them to get that info ASAP because it might change if the car is totaled or if it just gets repaired. If the repair cost is high just due to parts rarity, it might be a lot less pain than you think if you can show the value is high. I don’t think anyone wants this vehicle to get a rebuilt or salvage title.

RallyDarkstrike - Fan of 2-cyl FIATs, Eastern Bloc & Kei cars

> Jake - Has Bad Luck So You Don't Have To

RallyDarkstrike - Fan of 2-cyl FIATs, Eastern Bloc & Kei cars

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 14:37 |

|

Wait, what? How can it be total

ed, the paint looks scraped, but otherwise there doesn’t look to be much damage at all? 0_o Is there undercarriage damage?

|

Jake - Has Bad Luck So You Don't Have To

> RallyDarkstrike - Fan of 2-cyl FIATs, Eastern Bloc & Kei cars

11/14/2018 at 14:41 |

|

Do you know how expensive paintwork is?

|

RallyDarkstrike - Fan of 2-cyl FIATs, Eastern Bloc & Kei cars

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 14:46 |

|

Yeah, not cheap. I keep forgetting the bank still has a claim to it. If it wer

e

me mostly the bumper, you could always get a replacement, not bother to paint it for the time being and just run it that way, but I imagine there is a lot of paint damage on the quarter and hood?

Chariotoflove

> Jake - Has Bad Luck So You Don't Have To

Chariotoflove

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 15:00 |

|

Missed the original accident report. This sucks man. I hope your bank can help get you sorted out on the value . It shouldn’t be totaled.

Monkey B

> Jake - Has Bad Luck So You Don't Have To

Monkey B

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 15:22 |

|

there doesn’t appear to be any structural damage, that said I’m assuming parts prices are high? Get a few dealerships to give you a number sans damage and offer those to them as insurance companies do the least amount of research possible on this stuff. If you can prove it they are generally open to working with it. What’s the estimate at currently?

I missed the post on what happened.

|

Jake - Has Bad Luck So You Don't Have To

> Monkey B

11/14/2018 at 15:58 |

|

Travelers insurance uses CCC which finds “comparables” in the area and then uses some dicky algorithm to adjust that price up or down depending on options. Trade in value is like $3800.

The killer here is that 80% of the car is gonna need repainted.

|

Jake - Has Bad Luck So You Don't Have To

> Chariotoflove

11/14/2018 at 15:59 |

|

It probably will be. New bumper and fender, possibly new hood, then paint on all those parts and repaint the A pillars and roof.

That’s a shitload of work on a car that NADAs at $5400

|

Chariotoflove

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 16:01 |

|

Dammit, I know you’re right. That stuff can rack up fast. I remember the very first week I had my shiny new RX-8. I was so happy. I was in a McDs and I backed up into one of those landscaping boulders just below my field of view. The bumper was fine, but the paint work along to make it go away was $600 out of pocket.

V12 Jake- Hittin' Switches

> Jake - Has Bad Luck So You Don't Have To

V12 Jake- Hittin' Switches

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 16:43 |

|

If you can prove the real world value it’s possible that you can get your value adjusted higher. I could have bought a similar S600 with the am ount of money that insurance decided to fix mine with, but due to its condition they decided the actual value was close to twice NADA.

|

Jake - Has Bad Luck So You Don't Have To

> V12 Jake- Hittin' Switches

11/14/2018 at 17:06 |

|

Nope. Travelers uses CCC which uses their own algorithms and it’s the “Industry Standard” and can’t be argued with. Just went through this when my Miata was totaled two weeks ago.

|

V12 Jake- Hittin' Switches

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 17:16 |

|

RIP IS300 then :(. I can’t even imagine having both of my cars totaled within a month.

Jmvfeo

> Jake - Has Bad Luck So You Don't Have To

Jmvfeo

> Jake - Has Bad Luck So You Don't Have To

11/14/2018 at 22:17 |

|

$5,300 is how much I was payed a few months ago for my 2002 Lexus IS300 it had like 290,000 miles on it when I crashed.

I decided to keep the car and was charged less than $500 to keep it. M y damages were a broken headlight and broken bumper. Spent less than $800 dollars on the repairs.

pip bip - choose Corrour

> Jake - Has Bad Luck So You Don't Have To

pip bip - choose Corrour

> Jake - Has Bad Luck So You Don't Have To

11/15/2018 at 05:55 |

|

fix it up

|

Jake - Has Bad Luck So You Don't Have To

> pip bip - choose Corrour

11/15/2018 at 08:26 |

|

Bank owns it. Everything is sort of out of my hands.